Due to the fact that mobile houses depreciate in value with time, it can be more difficult to find a loan provider that provides produced house financing than if you were buying a conventional home. That said, there are still plenty of choices readily available. Simply be sure to do your due diligence to find the ideal one for you based upon your creditworthiness, your financial circumstance and your requirements and preferences.

A report released by the U.S. Census Bureau in 2015 discovered that a single-unit produced home offered for about $45,000 usually. Though the problem of getting a personal or home mortgage under $50,000 is a well-known problem that continues to disfavor low- and medium-income borrowers, adversely affecting the whole inexpensive housing market. In this post we're exceeding this problem and discussing whether it's much easier to get an individual loan or a conventional property home mortgage for a made house. A manufactured home that isn't permanently affixed to land is considered personal effects and financed with a personal effects loan, likewise described as belongings loan.

While a manufactured home titled as genuine residential or commercial property does not immediately ensure a traditional realty home mortgage, it does increase your opportunities of getting this form of funding, as discussed by the NCLC. However, getting a traditional mortgage to purchase a produced home is normally more difficult than getting an effects loan. According to CFED, there are three main factors (p. 4 and 5) for this: Though a manufactured house permanently attached to land is simply like a site-built building and construction, which can not be moved, some lenders incorrectly presume that a made house put on irreversible foundation can be relocated to another area after the setup.

Considering that a lot of lenders compare today's manufactured houses with previous mobile homes or take a trip trailers, they stay reluctant to use traditional home mortgage financing generally set to be paid back in thirty years. To deal with the impractical presumptions about the "inferiority" (and related depreciation) of produced houses, many lending institutions provide chattel loaning with regards to 15 or 20 years and high rates of interest. An essential however frequently ignored aspect is that the HUD Code has actually altered significantly for many years. Today, all manufactured homes https://www.storeboard.com/blogs/general/getting-my-what-does-leverage-mean-in-finance-to-work/5449634 must be developed to stringent HUD standards, which are equivalent to those of site-built building. Another reason that getting a made mortgage with land is more difficult than acquiring a goods loan is that lending institutions think that produced homes depreciate in worth due to the fact that they do not meet the current HUD foundation requirements.

Recently, CFED has actually concluded that "durable manufactured homes, correctly installed on a permanent foundation () value Go here in value" just as site-built homes. What's more, increasing numbers of lenders have begun to broaden the accessibility of conventional home mortgage funding to made house buyers, indirectly recognizing the gratitude in worth of the made houses attached permanently to land. If you're looking for an inexpensive financing alternative for a manufactured home set up on irreversible structure, do not just accept the first effects loan used by a loan provider, as you might certify for a standard home mortgage with much better terms. To read more about these loans or to discover if you qualify for a made mortgage with land, call our exceptional group of economists today.

MH Advantage combines features, like a deposit as low as 3%, with the lower price and adjustable finishes of modern manufactured houses. MH Benefit homes are developed to mix into traditional neighborhoods. MH Advantage homes have functions like lower profile structures, garages or carports, and drywall throughout. See the Seller Home Specifications for details. Appraisers pick the most appropriate equivalent sales, which unlike requirement MH may include sales of site-built houses. Confirming the house is qualified for MH Benefit is likewise easy for lenders: The appraiser will include images of the MH Advantage producer sticker labeland particular gain access to enhancements in the appraisal.

Some Known Questions About What Is Finance Charge On Car Loan.

MH Advantage brings cost effective financing to produced real estate with: A down payment as low as 3% Waived 0 - How long can you finance a used car. 50% LLPA, which suggests more homebuyer savings MI coverage equivalent to site-built houses.

Under the Title I program, FHA approved lending institutions make loans from their own funds to qualified customers to finance the purchase or refinance of a manufactured house and/or lot. FHA guarantees the lender versus loss if the customer defaults. Credit is given based upon the applicant's credit rating and ability to repay the loan in routine month-to-month installments. FHA does not provide cash; FHA guarantees loans in order to motivate mortgagees to lend. Title I produced home mortgage are not Federal Federal government loans or grants. The interest rate, which is worked out in between the customer and the lender, is needed to be fixed for the entire term of the loan, which is typically 20 years.

The home should be used as the primary residence of the debtor. For Title I insured loans, borrowers are not needed to buy or own the arrive on which their manufactured house is put. Rather borrowers might rent a lot, such as a site lot within a made house community or mobile home park. When the land/lot is rented, HUD requires the lessor to provide the manufactured property owner with a preliminary lease term of 3 years. In addition, the lease must supply that the property owner will get advance written notice of at least 180 days, in case the lease is to be ended.

Manufactured home only - $69,678 Produced home lot - $23,226 Produced home & lot - $92,904 twenty years for a loan on a made house or on a single-section produced home and lot 15 years for a manufactured house lot loan 25 years for a loan on a multi-section manufactured home and lot Manufactured houses are normally bought through dealers or retailers that offer the homes. The names of loan providers in your area which specialize in funding made houses can be acquired from local merchants. These merchants are listed in the yellow pages of your phone book. They have actually the needed application.

HUD supplies 2 types of customer defense. The debtor needs to sign a HUD Positioning Certificate concurring that the home has been set up and set-up to their fulfillment by the retailer before the lending institution can give the loan continues to the retailer. After moving in, the borrower can call HUD at (800) 927-2891 to get help about the problems with construction of the house. Have enough funds to make the minimum needed downpayment. Be able to show that they have adequate earnings to make the payments on the loan and fulfill their other expenditures. Plan to occupy the manufactured home as their principal home.

The house might be placed on a rental website in manufactured home park, supplied the park and lease contract fulfill FHA standards. The house may be positioned on a private homesite owned or rented by the borrower. Fulfill the Model Manufactured Home Installation Standards. Bring A 401(k) loan is a tool you can use to secure cash and then repay it in regular installations. These loans are typically interest-free. When you pay interest on them, it goes right back into your savings account, all set for you to access in the future. The downside is that you will lose on the return that your obtained funds could have created, had you left them in your account. If you default on any impressive loans, the Internal Revenue Service may choose that they are not tax-deductible, increasing your earnings tax expense. Finding a 2nd house is a difficulty, especially if you intend on purchasing in a location you do not understand much about.

They will be able to give you all the information you need to make a sound choice. Invariably, you will deal with unanticipated additional expenses when buying a 2nd house or trip home. Things like having to remodel the residential or commercial property or paying a company to handle it when you're not there all consume into your returns. You might likewise have to pay additional insurance costs if you rent it out. Regrettably, not everyone can manage to purchase a 2nd house upfront. The quantity that you can obtain will depend on just how much of your after-tax earnings already goes towards paying the home loan on your existing home.

Taxes on second houses vary from those on main houses. Again, this can eat into your returns and trigger you financial headaches if you do not completely understand it. You can't, for example, deduce second-mortgage interest from your gross income. When it pertains to funding your second house, therefore, you have plenty of choices. So long as you have sufficient wealth already, you can generally generate significant extra earnings from a 2nd residential or commercial property and enjoy it whenever you like. Related:.

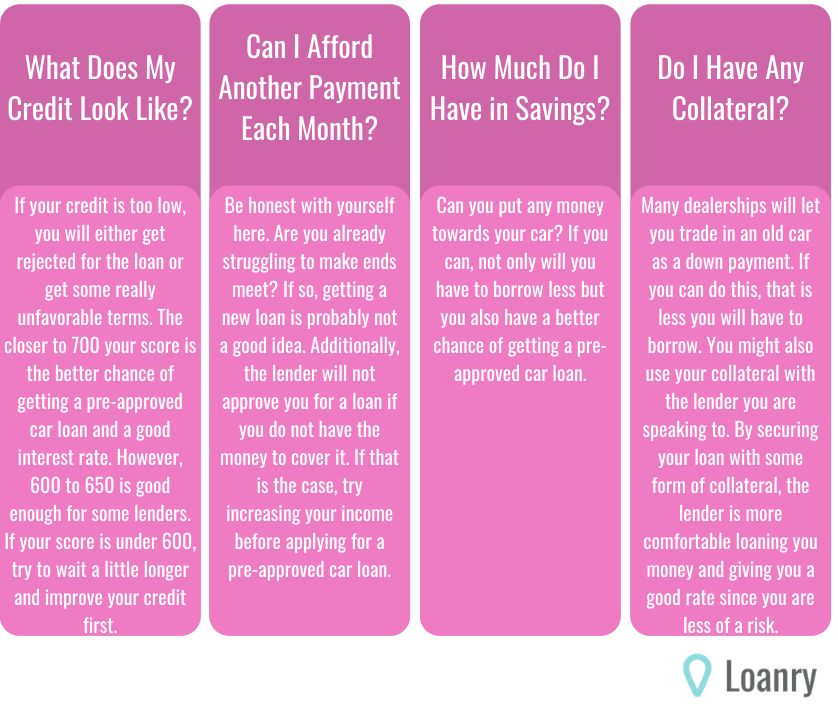

If you choose to take out another mortgage to pay for a second house, loan providers will look carefully at your debt-to-income (DTI) ratio to figure out whether you can handle 2 mortgage payments. A low DTI also works to your advantage because it assists you get approved for a lower interest rate on the loan. For 2nd homes, lenders prefer a DTI below 36%. If your DTI is high, you have a number of choices. You can pay off more financial obligation before buying another house, buy a less expensive home or increase the amount of your deposit. Some lending institutions desire a down payment of 10-20% on second homes, potentially more if it's simply an investment property. First, include up all the costs. Not simply the costs that go into the purchase, but the costs that may not be immediately apparent. These include your deposit and month-to-month mortgage payments, along with closing expenses, utilities, home taxes, insurance, landscaping, travel costs and other maintenance. On your primary mortgage, you might be able to put as little as 5% down, depending on your credit report and other aspects. On a 2nd home, however, you will likely need to put down at least 10%. Since a second home mortgage usually includes more monetary pressure for a property buyer, lending institutions typically look for a slightly greater credit rating on a second home loan.

Otherwise, the procedure of getting a 2nd house mortgage resembles that of a primary house mortgage. Just like any loan, you must do your research study, talk with multiple loan providers and choose the loan that works best for you. Prior to you look for a 2nd house mortgage, evaluate your credit rating, assets and income, just like a loan provider will. To buy a second house, you'll likely need money in reserve that might cover your home loan payments in case you have a short-term loss of income. Well-qualified people most likely requirement at least two months of reserves, while less-qualified applicants might require a minimum of six months of reserves.

Debt-to-income (DTI) requirements for a 2nd house mortgage may depend upon your credit history and the size Learn more here of your down payment. Typically speaking, the more you put down and the greater your credit history, the most likely your lending institution will enable a greater DTI. Some property owners might choose to offset their costs by leasing out their vacation houses when they're not using them. Doing this might breach your home loan terms because you are using the residential or commercial property as an investment instead of a true second home, resulting in higher threat to the loan provider. To qualify as a trip or second house, the residential or commercial foreclosure timeshare property must: Be resided in by the owner for some part of the year Be a one-unit home that can be used year-round Belong just to the buyer Not be leased, or run by a management firm You have a couple of alternatives to think about when making a deposit on your 2nd house.

If you have actually developed up enough equity in your main house, a cash-out refinance permits you to take advantage of that equity, particularly if your house has actually increased in worth because you bought it. Debtors with excellent credit can typically obtain approximately 80% of their house's existing worth (What jobs can i get with a finance degree). Before you go this direction, make certain you can manage the bigger regular monthly payment you'll now owe on your main house. A HELOC, or home equity credit line, on your primary house is another popular option. If you have enough equity in your primary home, you can get a credit line and utilize those funds to make a deposit on your second property.

Facts About What Is The Difference In Perspective Between Finance And Accounting? Uncovered

Purchasing a 2nd house may appear tough, but if you know what to anticipate and evaluate your finances, it might be simpler than you think (What is a consumer finance account). Keep these consider mind as you consider whether you can pay for a second home, and how to get a home loan for it.

">Visit this link a 1 year maker's service warranty if the system is brand-new. Be set up on a homesite that meets recognized local standards for website viability and has sufficient supply of water and sewage disposal centers offered. The earnings of a Title I manufactured home loan may not be used to fund furniture (for example, beds, chairs, sofas, lamps, rugs, and so on).